Thailand stands at a critical industrial crossroads, aggressively maneuvering to transform its decades-old identity from the “Detroit of Asia”—a hub of internal combustion engine manufacturing—into a premier regional base for electric vehicle (EV) production. Driven by the ambitious “30@30” policy, which mandates that 30% of all vehicles produced must be zero-emission by 2030, the nation has witnessed an unprecedented influx of foreign direct investment, particularly from Chinese automakers like BYD, Great Wall Motor, and MG. These investments, exceeding USD 4.2 billion by mid-2025, have fundamentally altered the competitive landscape, creating a vibrant but volatile market where EV adoption rates have surged to nearly 20% of new car sales, far outstripping regional peers. However, this rapid transition has triggered a fierce price war that has destabilized residual values and placed immense pressure on the legacy supply chain of over 2,500 parts manufacturers who must now adapt or face obsolescence.

THAILAND’S EV LANDSCAPE

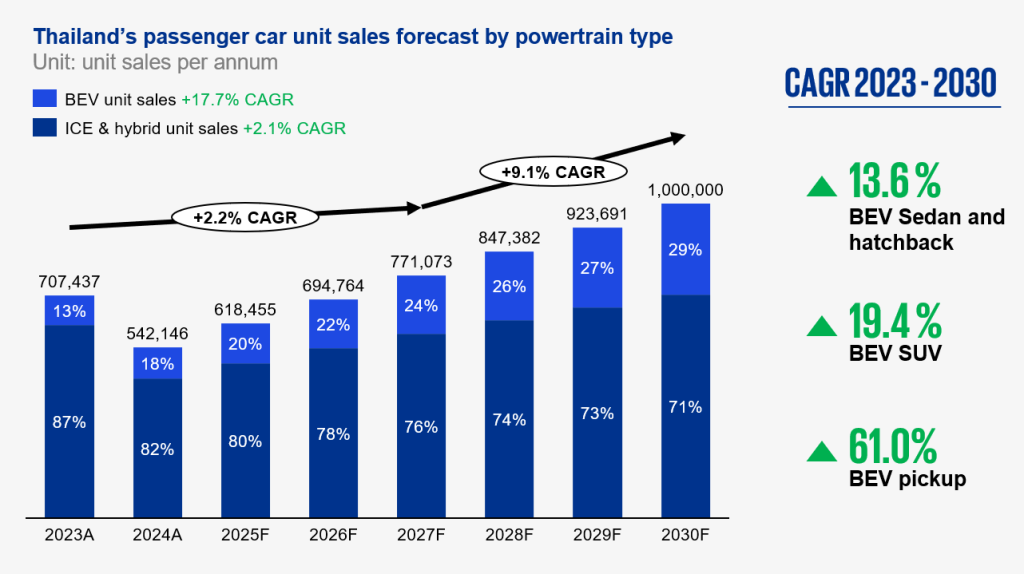

Thailandʼs electric vehicle (EV) sector is poised for significant expansion, fueled by favorable government policies, rising consumer interest, and a surge in foreign investment—especially from Chinese automakers (OEMs). Already a manufacturing powerhouse in Southeast Asia, Thailand is strategically leveraging its assets to dominate the regional EV market. These strengths include a robust supply chain, cost-effective labor, a prime geographic location for exports, and a business-friendly regulatory environment. While potential escalations in international trade wars and US reciprocal tariffs may introduce some short-term investment uncertainty, they are not expected to shake the industry’s strong fundamentals. The outlook is promising Battery Electric Vehicle (BEV) sales are projected to grow at a Compound Annual Growth Rate (CAGR) of 17.7%, climbing from 92,567 units in 2023 to roughly 290,000 units by 2030, capturing about 29% of the total market share. In terms of vehicle type, SUVs are expected to lead the pack due to their versatility, suitability for families, and adaptability to Thailand’s terrain. Sedans and hatchbacks follow closely behind, with hatchbacks gaining traction thanks to their compact size and affordable entry prices.

INFLUX OF THE BRANDS

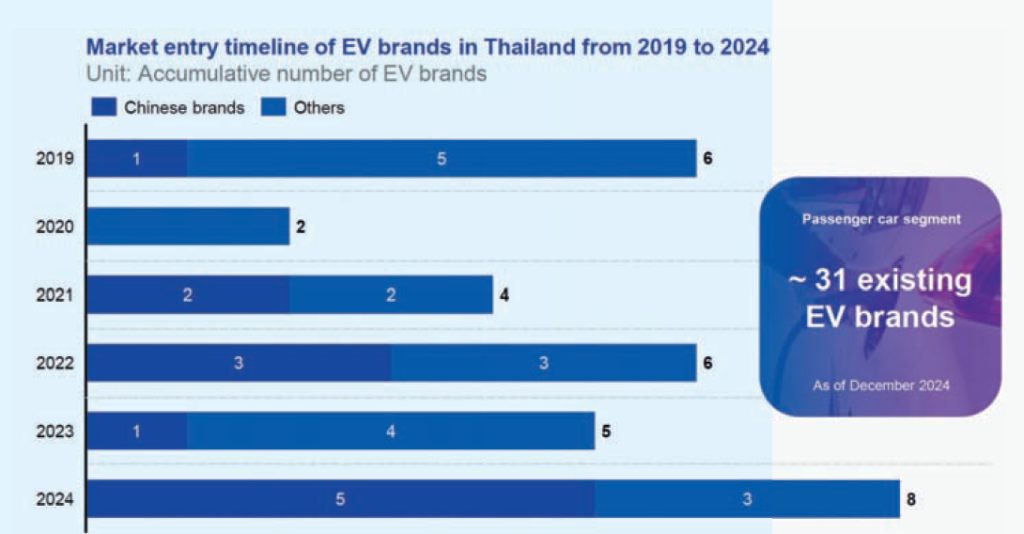

Since 2019, Thailandʼs automotive landscape has undergone a significant transformation as a wave of new electric vehicle (EV) entrants, primarily from China, challenges the long-standing dominance of Japanese incumbents. Leveraging global economies of scale and favorable trade agreements that exempt Completely Built-Up (CBU) imports from duties-privileges not extended to competitors from the US, Japan, South Korea, or Germany-Chinese OEMs have rapidly secured a strong foothold in the price-sensitive mass market. Among the 31 leading EV brands now present, approximately 12 are Chinese manufacturers such as BYD, GWM, MG, ZEEKR, and NETA, which utilize these systematic advantages to offer value-for-money vehicles, whereas Western brands like Tesla and BMW remain focused on the premium sector. However, this competitive edge faces potential headwinds under the new “EV 3.5” policy, which mandates a transition to local manufacturing with a production ratio of two locally assembled units for every imported unit by 2026, increasing to three-to-one by 2027. This mandatory shift from importing mass-produced units to establishing lower-volume local assembly lines is expected to increase cost structures, making it increasingly difficult for Chinese automakers to maintain the aggressive pricing strategies that drove their initial success.

THAILAND’S E-MOBILITY POLICY

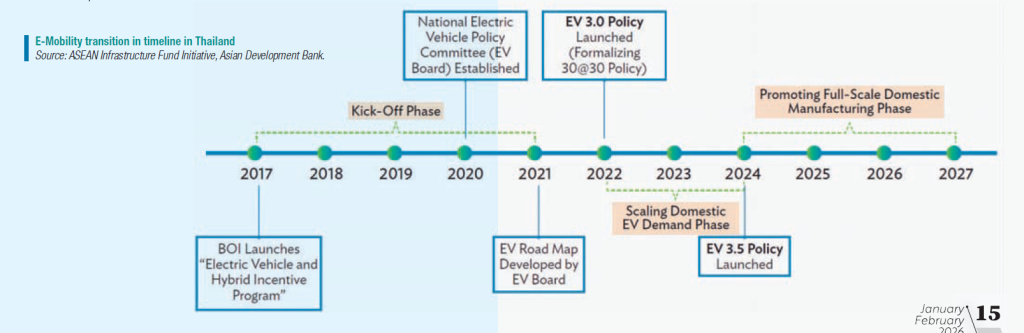

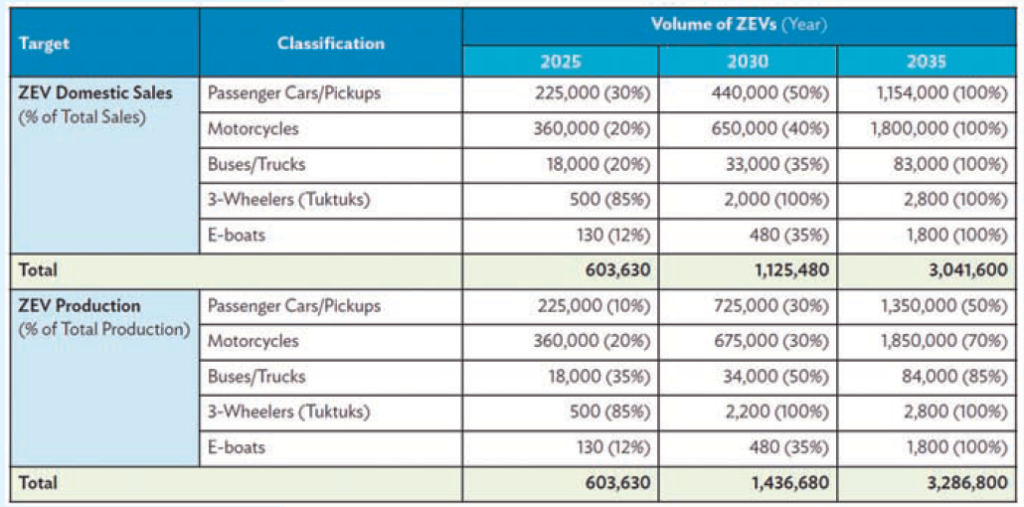

Thailand is pivoting from simply encouraging electric vehicle adoption to establishing itself as a regional manufacturing powerhouse. The policy landscape has evolved from the EV 3.0 phase, which kick-started demand through subsidies, to the current EV 3.5 framework (2024‒2027). This phase prioritizes industrial sustainability via stricter localization mandates- requiring manufacturers to offset imports with domestic production—while incentivizing local battery and component manufacturing. This strategy underpins the 30@30 target, aiming for zero-emission vehicles to comprise 30% of domestic auto production by 2030. Looking ahead, the Thailand E-Mobility Mission 2025‒2035 seeks to close critical ecosystem gaps, particularly in infrastructure and commercial transport. While passenger car adoption is surging, the roadmap addresses the urgent need to electrify public buses and heavy freight, sectors that have lagged due to insufficient targets. The plan outlines a comprehensive rollout to expand fast-charging networks beyond major cities and integrate renewable energy.

By combining supply-side mandates with nationwide charging accessibility and workforce reskilling, Thailand aims to achieve carbon neutrality by 2050 and secure its position as a self-reliant leader in the Southeast Asian EV market.

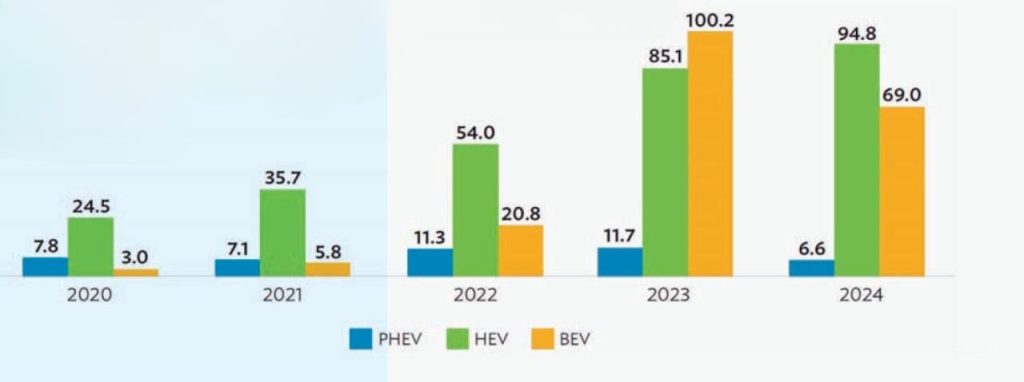

Driven by over a decade of supportive policies like the EV 3.0 and EV 3.5 frameworks, Thailand is rapidly transitioning toward electric mobility, currently dominated by Hybrid Electric Vehicles (HEVs) but witnessing surging growth in Battery Electric Vehicles (BEVs). With HEVs comprising over 60% of the electric fleet and BEVs growing at an impressive 143.6% annual rate, the government has set ambitious production targets, aiming for 30% of domestic vehicles to be electric by 2030, and established specific milestones for 2025, 2030, and 2035 across all vehicle segments. While electric cars are on track to meet these goals given their current growth trajectory, the electric motorcycle sector will require accelerated adoption measures to bridge the gap between current trends and the aggressive 2030 targets, likely following an S-curve adoption pattern as the market matures.

CONCLUSION

Thailand is launching a major 10-year plan called the Thailand E-Mobility Mission 2025‒2035 to completely reshape its automotive industry. Instead of just encouraging people to buy electric vehicles (EVs), the goal is to turn Thailand into a manufacturing powerhouse that builds EVs to sell to the world. To make this happen, the country is fixing the shortage of charging stations and expanding electrification to include buses and big trucks, not just cars. By updating its policies to focus on local production, Thailand aims to become the leader in the Southeast Asian EV market while hitting its goal of net-zero emissions by 2050.

Article By: Asst. Prof. Suwan Juntiwasarakij, Ph.D., Senior Editor & MEGA Tech