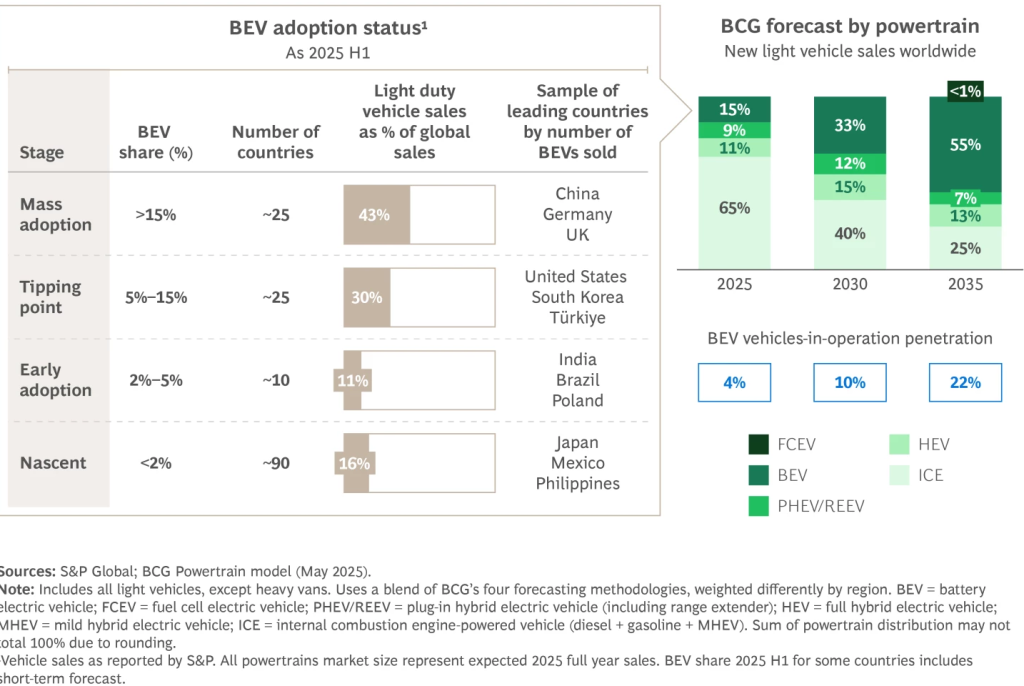

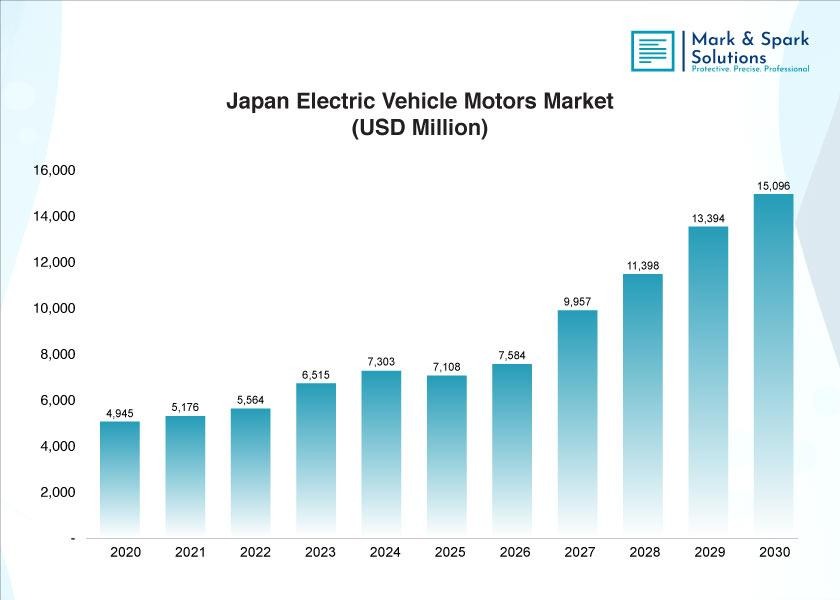

The global auto industry has entered a critical transition in 2026. The aggressive expectations from the early 2020s for electric vehicle (EV) expansion are now confronting the practical challenges of global market adoption. While macro indicators reflect substantial long-term momentum—such as a projected market growth from $0.67 trillion in 2025 to $0.75 trillion in 2026 and an 11.68% annual growth rate aiming for $1.30 trillion by 2031—the actual competitive reality is much more fragmented. For example, mature Western markets are experiencing demand stagnation for battery electric vehicles (BEVs) as consumers balance affordability, charging access, and everyday practicality. In contrast, China is currently leading the global market due to aggressive, subsidized manufacturing parity. Recognizing that battery cost parity remains several years off in the West, legacy automakers, particularly Japanese OEMs, are acknowledging that the transition is a long-term marathon, not a sprint. Attempting to compete directly with aggressive Chinese scale in the near term is viewed as financially risky, requiring a more agile, multi-pathway strategic approach to survive the current market conditions.

In response to stalling demand for pure electric vehicles (BEVs) and the severe financial losses suffered by Western automakers, Japanese carmakers are executing a pragmatic pivot back to hybrids (HEVs) and plug-in hybrids (PHEVs). Having avoided the costly “all-in” EV push that led to massive write-downs across the industry, companies like Toyota and Honda are capitalizing on their historical dominance in hybrid technology. Toyota has cut its 2026 BEV production target by 30% to a calculated 1 million units, while projecting a surge in hybrid production to 5 million units annually. Similarly, Honda is reducing its ten-year electrification budget from 10 trillion to 7 trillion yen, delaying new EV plants to prioritize shareholder returns and profitable hybrid sales. To protect shrinking profit margins, Japanese manufacturers are abandoning dedicated EV factories in favor of highly flexible assembly lines. These dynamic lines can build internal combustion, hybrid, and electric vehicles on the exact same footprint, allowing production to shift in real time with market demand. Furthermore, the industry is seeing unprecedented cross-company collaboration—such as Honda sourcing hybrid batteries from Toyota, and Nissan sharing powertrains with American automakers. This collaborative approach allows them to deploy proven technologies at scale while preserving the massive capital required for the fully electric era of the 2030s.

As the auto industry shifts from mechanical engineering to software and artificial intelligence, Japanese automakers are realizing they can no longer fund the future alone. To survive the staggering costs of developing hybrids, EVs, and autonomous driving tech simultaneously, the sector is aggressively consolidating. Most notably, Nissan, Honda, and Mitsubishi have forged a historic alliance to become the world’s third-largest automotive bloc by 2026. This partnership is designed to slash R&D costs by standardizing software platforms, pooling capital for battery procurement, and jointly engineering next-generation EV components. Simultaneously, the industry is seeing a massive surge in tech-focused mergers and acquisitions. Instead of simply buying market share, Japanese OEMs are acquiring semiconductor and AI startups to compete with digitally native giants like Tesla, whose valuation is driven by its integrated software and energy ecosystems. With advanced driver-assistance systems (ADAS) expected to dominate sales by 2030, vehicle software is no longer an add-on; it is the core product. To protect profit margins from volatile car sales, these automakers are pivoting toward the highly lucrative aftermarket. By transforming into software-enabled service providers—offering digital support, predictive maintenance, and data monetization—they are securing the stable, recurring revenue needed to fund the capital-intensive manufacturing realities of the 2030s.

The automotive center of gravity in Southeast Asia is undergoing a violent geopolitical shift. Thailand, long the undisputed “Detroit of Asia” where Japanese automakers held a 90% market share, has rapidly become the frontline against Chinese industrial expansion. Driven by saturated home markets and looming US-Mexico tariff threats, Chinese giants like BYD, GWM, SAIC, and Changan are aggressively executing a “China+X” strategy to build alternative export bases in the region. Lured by Thailand’s EV 3.5 policy—which mandates local production in exchange for lucrative consumer subsidies—these brands have completely disrupted the market. By the first quarter of 2025, EV market share in Thailand skyrocketed to 40.2%, crushing the government’s 30% target for 2026 and driving Japanese market dominance down to just 69%. Flooding the market with subsidized, tech-heavy EVs priced under 1 million THB (with dealer discounts up to 19%), Chinese brands have ignited a brutal price war. This deflationary pressure has forced Japanese OEMs into a painful defensive retreat: Subaru is exiting local production, Suzuki is shuttering its Thai plant by the end of 2025, and Honda is halving its manufacturing capacity by consolidating two facilities into one. To survive this onslaught, Japanese automakers are leveraging their established brand equity and pivoting hard toward localized hybrid vehicles, which currently account for 62% of the Thai EV market, perfectly tailoring their strategy to emerging regions where pure EV charging infrastructure remains scarce.

Instead of bleeding capital in a low-margin price war over current battery technologies dominated by Chinese giants, Japanese automakers are executing a high-stakes “leapfrog” strategy. They are betting their ultimate EV future on the commercialization of All-Solid-State Batteries (ASSBs). Recognizing the physical limitations and thermal risks of today’s liquid-electrolyte batteries, Toyota—backed by the Japanese government and in partnership with energy giant Idemitsu Kosan—is aiming to launch its first-generation solid-state EVs by 2027–2028. These next-generation vehicles promise to shatter current limitations, delivering up to 1,000 kilometers (620 miles) of range and an ultra-fast 10-minute charge time, with a second-generation architecture already targeting 1,200 kilometers (745 miles). This calculated move perfectly explains Japan’s apparent sluggishness in the current EV race. By intentionally withholding massive investments from gigafactories dedicated to soon-to-be-obsolete battery tech, companies like Toyota and Nissan are preserving their capital for the true technological battleground of the 2030s. If successfully scaled, ASSBs will entirely eliminate consumer “range anxiety,” drastically reduce vehicle weight, and allow Japanese manufacturers to reclaim global dominance by instantly rendering today’s electric vehicles technologically inferior.

CONCLUSION

The global pivot toward electric vehicles (EVs) is triggering an existential crisis for Japan’s deeply layered automotive supply chain. Because EVs require significantly fewer mechanical parts than internal combustion engines, traditional suppliers are rapidly losing essential manufacturing volume. This technological shift, compounded by acute labor shortages and a weak yen, drove Japanese corporate bankruptcies to a 13-year high of 10,300 in 2025, devastating vulnerable lower-tier manufacturers. This systemic fragility is now spilling over into critical overseas hubs like Thailand, threatening over 1,600 local auto parts companies. Compounding the threat, Chinese automakers are leveraging vertically integrated supply chains in ASEAN to undercut traditional Japanese component prices by 20% to 30%. Forced to compete, Japanese automakers are demanding brutal 30% cost reductions from their own networks, pushing legacy vendors to the brink of insolvency or distress sales. To survive this historic industrial contraction, Tier-1 giants like Denso and Aisin are actively orchestrating industry-wide consolidations, acquiring distressed assets, and radically pivoting their focus from mechanical hardware to software, electronics, and lucrative digital aftermarket services.

Article By: Asst. Prof. Suwan Juntiwasarakij, Ph.D., Senior Editor & MEGA Tech